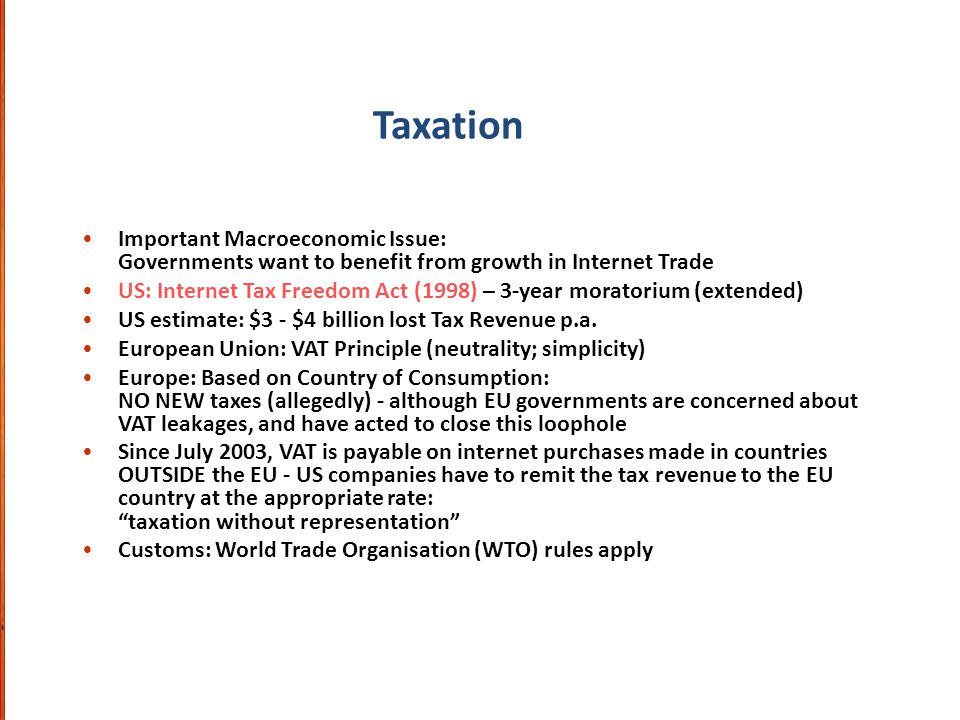

internet tax freedom act 1998

Originally enacted in 1998 as a temporary moratorium barring federal state and local governments from imposing internet access taxes as well as multiple or discriminatory taxes on electronic commerce ITFA was renewed eight separate times before being made permanent in 2015 under the Trade Facilitation and Trade Enforcement Act of 2015 Act. ITFA which prohibited states and localities from applying taxes on internet access or imposing discriminatory digital-only taxes became permanent in 2016 but included a grandfather clause that allowed states with taxes existing before 1998 to keep that.

![]()

Didn T The Internet Tax Freedom Act Itfa Ban Taxes On Sales Over The Internet Sales Tax Institute

105277 text PDF on October 21 1998 by President Bill Clinton in an effort to promote and preserve the commercial educational and informational potential of the Internet.

. Online sellers are still required to collect sales tax when selling items to buyers in states where you have sales tax nexus. The item Internet Tax Freedom Act of 1998. 1998 The Internet Tax Freedom Acts Advisory Commission on Electronic Commerce.

Moratorium on Certain Taxes - Prohibits a State or political subdivision thereof from imposing the following taxes on Internet transactions occurring during the period beginning on October 1 1998 and ending three years after the date of enactment of this Act. 1 Internet access taxes imposed under specified State. While the Internet Tax Freedom Act ITFA and its permanent counterpart PIFTA prevents states from imposing taxes on things like actually accessing the internet they do not have anything to do with eCommerce sales.

The law bars federal state and local governments from taxing Internet access and from imposing discriminatory Internet-only taxessu. This law placed a moratorium on the special taxation on the internet. The Internet Tax Freedom Act of 1998 ITFA.

A AMENDMENT- Title 4 of the United States Code is amended by adding at the end the following. Back then we used it predominately for email. Preserving Flexibility to Consider All Options by Michael Mazerov Summary The Internet Tax Freedom Act ITFA S.

The Internet Tax Freedom Act ITFA Title XI of the Omnibus Appropriations Act of 1998 was approved as HR. MORATORIUM ON CERTAIN TAXES. Congress voted to pass the legislation.

ITFA prohibits Internet access taxes multiple taxation of a single transaction by more than on taxing jurisdiction and discriminatory taxes that do not apply to offline purchases. 3529 including cost estimate of the Congressional Budget Office represents a specific individual material embodiment of a distinct intellectual or artistic creation found in Indiana State Library. The act made permanent a temporary moratorium on such taxes that has been in placethanks to multiple short-term extensionssince the Internet Tax Freedom Act of 1998 ITFA.

1 1998 when the US. 2 In addition to. Internet Tax Freedom Act - Title I.

October 9 1998 Web posted at 1125 AM EDT by Nancy Weil IDG -- The US. Jun 17 1998. The Act was intended to increase Internet use in the United States.

The Internet Tax Freedom Act of 1998 ITFA. TITLE XIMORATORIUM ON CERTAIN TAXES SEC. Notably the new act phases out a grandfather clause that has protected a handful of states Texas is among them allowing those states to tax Internet access despite the general.

Internet Tax Freedom Act Legislation in the United States originally passed in 1998 and renewed several times since that prohibits state and local governments from taxing the use of the Internet. 105-277 imposed on state and local governments a three-year moratorium from October 1 1998 to October 1 2001 on 1 new taxes on Internet access and 2 multiple or discriminatory taxes on electronic commerce. Congress extended the ITFA.

Internet Tax Freedom Act of 1998 Title XI of the Omnibus Appropriations Act of 1998 Pub. It also established the Advisory Commission on Electronic Commerce. 4328 by Congress on October 20 1998 and signed as Public Law 105-277 on October 21 1998.

The Internet Tax Freedom Act was first enacted on Oct. For example states and municipalities may not tax e-mails or bandwidth use. The Act placed a three-year moratorium on any new taxes on Internet access fees and prohibited multiple and discriminatory taxes on electronic commerce.

The Internet Tax Freedom Act formerly known as S442 now Title XI of PL. This title may be cited as the Internet Tax Freedom Act. CHAPTER 6--MORATORIUM ON CERTAIN TAXES Sec.

The managers amendment that will. This Act may be cited as the Internet Tax Freedom Act of 1998. For those of you that can remember back this far the Internet Tax Freedom Act was signed into law in 1998.

105-277 the Omnibus Appropriations Act of 1998 reproduced below establishes the Advisory Commission on Electronic Commerce. Senate voted Thursday 96 to 2 to approve a bill that places a prohibition on. Report to accompany HR.

442 may be brought to the Senate floor again in the next few days. According to Senate Report 105-184 Congress exercised. 1 taxes on Internet access unless such tax was generally imposed and.

Internet Tax Freedom Act of 1998 - Prohibits for three years after enactment of this Act any State or political subdivision from imposing assessing collecting or attempting to collect taxes on Internet access bit taxes or multiple or discriminatory taxes on electronic commerce with exceptions for. The Internet Tax Freedom Act ITFA enacted in 1998 was intended to protect the developing internet technology. To establish a national policy against State and local interference with interstate commerce on the Internet or online services and to excise congressional jurisdiction over interstate commerce by establishing a moratorium on the imposition of exactions that would interfere with the free flow of commerce via the Internet.

On 1 st October 1998 the US government enacted the Internet Tax Freedom Act ITFA with the intent to further promote and develop the internet technology. Advisory commission on electronic commerce. The ITFA put a bar on the states and the localities from imposing taxes on internet access.

The 1998 Internet Tax Freedom Act is a United States law authored by Representative Christopher Cox and Senator Ron Wyden and signed into law as title XI of PubL. As first enacted on October 21 1998 the ITFA imposed a three-year moratorium on the ability of state and local governments to impose taxes on internet access and certain internet transactions to the extent permitted by the Constitution and any other federal law in effect on that date. At that time the Internet was a start-up and the thought was that there needed to be a way to encourage people to use the Internet.

Internet Tax Freedom Act ITFA The ITFA was enacted in 1998 as a 3-year moratorium preventing governments at the local state and federal levels from imposing transaction taxes on internet access one of the exceptions being that states already taxing internet access as of October 1 1998 were grandfathered in. 105-277 imposed on state and local governments a three-year moratorium from October 1 1998 to October 1 2001 on 1 new taxes on Internet access and 2 multiple or discriminatory taxes on electronic commerce.

2

Ethical Legal And Public Policy Issues In E Business Ppt Download

What Is The Internet Tax Freedom Act Howstuffworks

Didn T The Internet Tax Freedom Act Itfa Ban Taxes On Sales Over The Internet Sales Tax Institute

Freedom Of Expression And The Internet

Pdf Pros And Cons Of E Commerce Taxation

Pdf E Commerce And Tax Revenue

What Is The Internet Tax Freedom Act Howstuffworks

Controversial Internet Tax Freedom Act Becomes Permanent July 1

Pdf Greater Freedom In The Cyberspace An Analysis Of The Regulatory Regime Of The Internet In Malaysia

Freedom Of Connection Freedom Of Expression The Changing Legal And Regulatory Ecology Shaping The Internet

2

2

Pdf E Commerce Taxation And Fiscal Policy Perspective The Case Of Indonesia

2

![]()

Didn T The Internet Tax Freedom Act Itfa Ban Taxes On Sales Over The Internet Sales Tax Institute

2

Pdf Transforming The Internet Into A Taxable Forum A Case Study In E Commerce Taxation

2